We are in the dog days of summer: Kids are out of school, Canadians are travelling abroad and up to cottage country. Things appear normal but….

Ever since March 2020, the Government and Bank of Canada have printed and stimulated the economy to keep it afloat. In the fall of 2021 signs of persistent inflation were clear however neither Bank of Canada or the government stopped their stimulus policy.

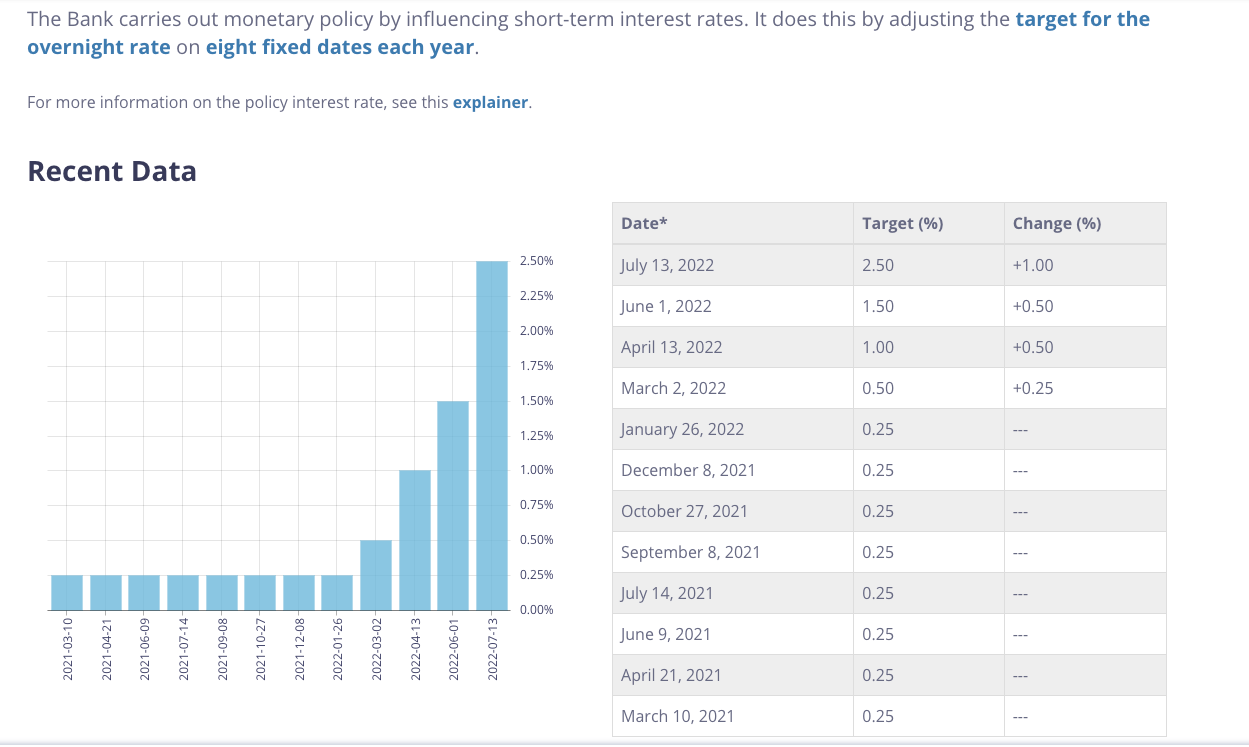

Move forward to July 2022 and we are in an aggressive inflation control period. Bank of Canada increased its benchmark rate (which sets the prime rate for variable mortgages and lines of credit) by a full 2.25% since March 2nd. This is the most aggressive increase in history with more hikes to come!!

Source: bankofcanada.ca

Toronto Real Estate: Do We Have A Problem?

Real estate is sensitive to cost of borrowing (mortgage rates). Since March 2022, the real estate market has been slowing down: Less appointments to see homes, less offers, very few offer presentation dates (where offers are accepted on a specific date) and more homes being relisted at a new price.

Are we in a correction? Let’s look at data and different perspectives.

Note: All figures below are from Toronto Regional Real Estate Board

Detached 416 average price Dec 2020: $1,475,758

Detached 416 average price June 2022: $1,737,012 (17.7% higher than Dec 2020)

Semi-detached 416 average price Dec 2020: $1,160,108

Semi-detached 416 average price June 2022: $1,343,378 (15.8% higher than Dec 2020)

Central 416 condo average price Dec 2020: $669,612

Central 416 condo average price June 2022: $809,894 (21% higher than Dec 2020)

Will prices fall by 15-20%? Time will tell but does it matter? Let’s look at the real estate market from 4 different perspectives:

1. Buyers Earlier than Dec 2020

You have done well. Bought into the market before prices took off and you probably have a very low mortgage rate. Keep calm and carry on.

2. Buyers Between Jan 2021 and March 2022

You probably were involved in multiple offers, might have lost on a few homes however you got the home you wanted and have a low mortgage rate. Keep calm and carry on since you won’t think about moving for a long time.

3. Buyers Between April 2022 and June 2022

You probably got mentally ready for multiple offers and a competitive market but were surprised with the lack of competition from other buyers. You got the home you wanted and you either had lower mortgage rate pre-approved or your mortgage rate was higher than you thought when started looking. Keep calm and focus on mortgage paydown. Moving? What’s moving? It’s not even a thought for a long loooong time.

4. Real Estate Investors

Whether your bought prior to Dec 2020 or recently the rental market is on fire and will continue to be strong for the following reasons:

Some buyers are being pushed out of the market due to higher mortgage rates

People continue to move back to the city as working from the office is returning whether hybrid or full time and the vibrant city lifestyle has come back

Less rental supply: Tenants who moved in the past 2 years are not moving, they got in at low rental prices

New supply delays: Supply chain issues, labour disruptions and rising construction costs are delaying the completion of new rental stock

What Happens Next?

The Bank of Canada sole focus is to bring inflation within the target range of 2-3%. I am skeptical of getting there since the inflation we are experiencing is due to the following:

Supply chain issues: To this day, China is under rolling lockdowns to control the spread of the virus. Bank of Canada has no influence on supply chain restrictions

Oil: Petroleum is a commodity controlled by OPEC. Bank of Canada has no influence on OPEC pricing

Russia/Ukraine: Again Bank of Canada has on influence

Bank of Canada bond buying: They have stopped the bond buying program which is a good thing to slow down stimulus

Federal Government Stimulus: I hope Ottawa controls its spending. Bank of Canada has no influence on Federal budgets but hopefully someone is listening

Bank of Canada is taking a sledge hammer to the demand side of the equation since it has no control of supply. Time will tell what the sledge hammer will do to the economy

My Perspective

We are in a period of aggressive change and more is to come. Humans are not good with change. This is like an airplane going through a turbulent patch, most passengers hold on tight till the plane passes through into steady and predictable skies. Moving forward, buyers and sellers will hold on tight, sit on the sidelines till the Bank of Canada indicates it is done with rate hikes and we are in a steady economic state. This is when more buyers and sellers will jump back in.

Two Final Points

Immigration is at approximately 450,000 newcomers per year. Once the economy stabilizes this will continue to contribute to strong demand and lack of housing supply. Price appreciation will be back in the headlines. Old news will be new news!!

House prices only matter when you sell. No need to stress about “average” Canadian house price. Real estate is local and it ONLY matters when you sell your home.

“This is your captain, fasten your seatbelts and hold on tight for the bumpy ride ahead”.

Till next time….