Another year comes to a close. 2015 has been a very active real estate market and the numbers don't lie.

Your mortgage is up for renewal or you just bought a home and it is time to decide: fixed mortgage or variable mortgage. Both options are at historic lows, which sounds like a broken record since the economic collapse of 2008. With 5 year fixed rates hovering around 2.89% and variable mortgages at prime less 0.6%, either option is attractive. But how do you choose? The answer is in oil prices.

With oil prices collapsing from $140 per barrel to $45-$50 range in the last 6 months, Canada's GDP growth will slow down and there are talks of Alberta going into recession, yes the "R" word. Over the last 4 years, Alberta has been carrying the country with its economic growth. As Alberta slows down, inflation will be lower, unemployment will be higher (in Alberta, NewFoundLand and Saskatchewan).

Slower economic growth (GDP and employment) will lead to lower inflation, below 2-3% target range for the Bank of Canada which would keep prime rate at current levels. If the economy shrinks, the Bank of Canada will cut prime rate to stimulate economic growth (as I write this post, the Bank of Canada has surprised the market by cutting the benchmark rate by 0.25%. Effective tomorrow, prime rate is 2.75%!)

Until the economy returns to "its full capacity" which the Bank of Canada is predicting to be late 2016, or later in my opinion, the benchmark rate which drives prime rate will probably not increase till then.

So, as oil prices go, so does the Canadian economy.

Buying an investment property is similar to buying a business; it needs to cash flow. Would you buy a business that loses money on a monthly basis? Probably not and you shouldn't buy an investment property that negative cash flows.

Now that we agree cash flow is critical, what should you do with the monthly cash flow surplus?

Let's assume the property cash flows after expenses and reserve fund allocation, $500. We encourage our clients to allocate a minimum of 8% of rental income for repairs, maintenance and vacancy allowance. For a property that generates $3,500 monthly, $280 is set aside.

There are 2 options to consider for the net $500 monthly cash flow:

1. Prepay investment property mortgage

2. Prepay principal residence mortgage

Assume your principal residence mortgage balance is $400,000 borrowed at 2.99% and amortized over 30 years with a monthly payment of $1,680.28. By diverting $500 monthly into your principal residence, the mortgage amortization is reduced to 20.42 from 30 years, saving you 9.6 years or $193,568 of mortgage payments.

Imagine having no mortgage payment!

Another factor to consider is tax efficiency (disclaimer: consult a professional accountant for tax advice, we are not accountants). The interest portion of a principal residence mortgage, for majority of homeowners, is not tax deductible. Whereas the interest portion of the investment property mortgage is tax deductible. A sound financial strategy is to pay off non tax deductible debt first.

Once the principal residence mortgage is paid off, use the rental property surplus to pay down the investment property mortgage to increase cash flow and pay it off ahead of the original amortization.

Questions? We can be reached via email or social media.

Buying a house, doing some work to it and selling it for $100,000 profit a few months later sounds like a lucrative proposition, but is it really?

Canada Revenue Agency will tax the profit as income not capital gains. In this instance, the full $100,000 profit would be taxed at your marginal tax rate.

Here is an example of why I prefer to flip the house.....later: Buy, Add Value, Refinance (BAR) then hold

If property is sold after 5 years, only 50% will be taxed at your marginal tax rate. Assuming a sale price of $675,000, only $87,500 out of the $175,000 ($675,000-$500,000 divided by 2) would be taxed at your marginal tax rate. Disclaimer: Always consult a professional accountant who specializes in real estate investment to guide you through CRA's rules and regulations. Capital Costs Allowance are not taken into consideration in this example.

To summarize the 2 options:

1. Sell Now: $100,000 profit taxed at marginal rate

2. Sell in 5 Years: $237,438 profit (difference between property value and remaining mortgage balance) plus $41,588 in cash flow over 5 years, only $87,500 taxed at marginal tax rate

Advanced real estate investor tip: Don't sell the property after 5 years, refinance it to pull equity to buy another investment property which would defer paying capital gains taxes to a future date and build portfolio by acquiring another investment property.

To answer your questions or to put your financial freedom plan, we can be reached via email or social media.

You bought an investment property 5 years ago and it's time to renew the mortgage. Should you renew the mortgage or refinance to pull equity to buy another investment property? This is a common question we get from our investor clients (This question is applicable to your home mortgage as well).

Here is an example to best illustrate the options:

Current Property Value: $720,000

Mortgage Balance: $465,000

Option 1 - Pull Equity to 80%: new mortgage $576,000 amortized over 35 years. Access $111,000 of equity to acquire another investment property (35 year amortization is available for investment properties)

Option 2 - Renew mortgage at current remaining amortization and mortgage balance remains unchanged at $465,000

If the real estate investor is in acquisition phase, it is best to proceed with option 1. This also provides a tax advantage; the interest costs for the additional $111,000 are tax deductible since it is used for investment purposes (disclaimer: consult an accounting professional for tax advice). A key point to consider when deciding how much equity to pull out of the investment property is to stress test the cash flow using higher interest rates to ensure the investment property will not negative cash flow in the future.

If the real estate investor has completed acquiring the number of properties required per the plan, it is best to proceed with option 2 to pay off the investment properties and increase passive income.

Having a plan upfront helps you, the real estate investor, in knowing how many properties are required to achieve your long term financial goals and deciding what to do at mortgage renewal time.

Questions? We can be reached via email or social media.

Over the years working with real estate investors, I have come across very interesting answers when I ask "How many investment properties do you need to buy?" I have heard from 1 property to 40 properties, 1 every year for the next 5 years, don't know... Most stumble when I ask why? It starts with why. Simon Sinek explains the importance of starting with why in his TED Talk

There are many reasons for buying investment properties, here are some:

Retirement income

Fund children's post secondary education

Job replacement (one spouse might be considering leaving their job)

Supplemental income

Family legacy

Full time real estate investor

Investment diversification (real estate and stock market)

Once a reason or multiple reasons are chosen, determining how much monthly income the investment properties are to generate is the next step. This goal can be achieved via different investment properties options (single family, duplex, multi-family, commercial....) and various geographic locations.

To complete "why invest in real estate" analysis, reverse Engineer the number of properties you need and have your personalized "how and where" plan developed, click here.

Homeowners are taking advantage of historic low interest rates whether they are fixed, around 3%, or deeply discounted variables around prime less 0.5%. Majority of homeowners and real estate investors choose a 5 year term, but what happens in the future if it is required to increase the mortgage amount for the purpose of debt consolidation, equity take out for investment purposes, or moving to a new home?

Example: Property value $480,000. Current mortgage balance is $250,000 at 3.09% with 3 years remaining till maturity and the homeowner wants to borrow $150,000 to buy an investment property. There are 3 options for the homeowner to entertain:

The above illustrates the options for a fixed mortgage holder. The options are different for variable mortgage holders:

One thing to look out for is the fine print detail for no frills mortgages (ultra low rates) as some might restrict the homeowners ability. For example, BMO's 2.99% offer allowed the homeowner to refinance only with BMO and did not allow adding a HELOC. Since the homeowner has no negotiating power they are at the mercy of the bank when it comes to interest rates.

There is more to mortgages than interest rates. Rates are the cost of getting into the mortgage, however the fine print can cost thousands more.

To navigate through the mortgage minefields and for a hassle free transparent experience please contact Nawar.

It is that time of year again....spring market. This is when the majority of real estate transactions occur and hence when the banks tend to get aggressive on mortgage pricing to gain market share. Another 2.99% offer was made by BMO which was in the headlines across various media outlets. My objective in writing this article is to explain the fine print of BMO's mortgage. In 2014 homeowners ought to expect more transparency and explanation from their mortgage professional or bank employee.

Here are the fine print details of the 2.99% offer:

It is important for homeowners to sit with their mortgage professional and ask about the cost of getting into the mortgage (interest rate) and inquire about the costs of getting out of the mortgage (penalties, portability, restrictions). A mortgage is one piece of the puzzle in a homeowner's financial plan and it is important to ensure the right product is chosen based on features and not just rates.

The mortgage qualifying rate is used to qualify all variable mortgages and fixed mortgages of 1-4 year term. The Bank of Canada updates the mortgage qualifying rate (MQR) every Monday at 12:01am. 5 year fixed or longer fixed terms qualify using the contract rate (the actual borrowing rate). Here is an explanation:

Assumptions

Maximum fixed mortgage: $577,000 (Purchase price: $721,250) Maximum variable mortgage: $466,000 (Purchase price: $582,500)

One way to increase the purchase power of a variable or fixed mortgage is obtain a 35 year amortized mortgage. Once the homeowner takes possession of the home, they can set the payment at the 30 year amortization level to avoid paying additional interest over the life of the mortgage.

To find out what you qualify for and a have a winning strategy for bidding wars, please contact Nawar.

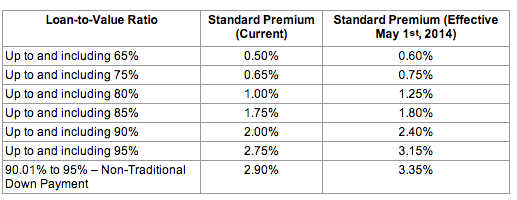

On February 28, 2014, CMHC announced mortgage insurance premium will increase effective May 1, 2014 for homeowners, self employed and 1-4 rental properties. Here is a chart of the current and new insurance premiums for owner occupied homes

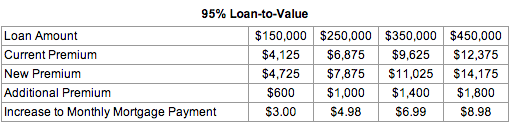

What exactly does this increase translate into dollars and cents? Here is an example based on 5% downpayment, 3.49% mortgage amortized over 25 years

As you can see the increase is moderate ($8.98 per month) and should be manageable by homebuyers. It will be interesting to see what happens in the future since CMHC stated they will review insurance premiums annually and make announcements in the first quarter moving forward.

Genworth wasted no time in announcing similar increases to their premiums effective May 1, 2014. Canada Guaranty took a few days to mull over their decision but they will increase their insurance premiums as well.

[contact-form subject='I Have A Question...'][contact-field label='Name' type='name' required='1'/][contact-field label='Email' type='email' required='1'/][contact-field label='Comment' type='textarea' required='1'/][/contact-form]

Referrals are still the primary method of getting introduced to a mortgage broker when buying a home or an investment property, however more and more Canadians are searching for mortgage brokers online. Borrowing hundreds of thousands of dollars is a serious undertaking and requires due diligence. Based on my years of experience here is a checklist of how to find a trustworthy mortgage broker.

Online Presence: Everyone, well pretty much everyone, has a website nowadays. However, are they active in publishing material relevant to the market? Are they experts in a niche market (real estate investment, self employed, first time home buyers, bad credit, private mortgages....) or are they the jack of all trades? Going through their website you will get a good feel if they are experts in a specific field.

Strategy vs No Strategy: Quoting rate requires no skills, afterall most brokers and lenders have the same rates with a possible difference of up to 0.1% ($100 for every $100,000 per year). Unfortunately, obtaining a mortgage licence is easy; one course, a few hundred dollars and off you go! If a broker or agent is only quoting rates without explaining the following, run away:

Pros and cons of each product

How each product helps you achieve your financial goals

Fine print terms (penalties, mortgage features)

A plan to pro-actively manage the mortgage post funding

Execution: A financial planner engages their clients on an ongoing basis to adjust their portfolios as economic conditions and clients' lifestyle change, why wouldn't you expect the same from your mortgage broker? Building net worth is achieved through 2 ways: 1/ increasing assets and 2/ decreasing bad debt. How will the mortgage broker track your mortgage and keep you informed? Why not have a debt manager on your team?

Full Time vs Part Time: Since mortgage agents have a low barrier of entry, there are some out there who operate on a part time basis. There is nothing wrong with someone building their business to transition full time into the profession, but would you trust a part time lawyer, a part time doctor, a part time real estate agent or a part time contractor?

Experience: I'm into sports, so I'll use a sports analogy: great coaches used to be players in the past. If you are looking to invest in real estate, shouldn't you engage a mortgage broker who invests in real estate, whose been through the ups and downs? If you are self employed, shouldn't you approach a full time self employed mortgage broker who personally experienced the challenges of getting mortgage financing? If you are a first time buyer, shouldn't you meet with a mortgage broker who had a terrible experience getting a mortgage for their first home?

Job Interview: I view hiring a mortgage broker as applying for a job. You probably can recall going for a job interview, where the interviewers asked lots of questions and based on your answers (and references) got a gut feel for you. Hiring a mortgage broker is the same, use the above information to ask questions and get a good gut feel for who you should hire. You are trusting a professional with hundreds of thousands of dollars.

If you are buying your first home, an investment property or you are self employed and looking to interview a professional mortgage broker, please contact me.

I have to share this personal experience since it resembles what I deal with on a daily basis with my mortgage clients. My home and auto insurance policies have been with a company for years now until I got my renewal letter a few weeks ago. The jump in insurance premium caught my attention especially since my wife and I are responsible drivers: we have 2 young children, and our records have been impeccable; no tickets, no violations, no accidents.....Usually I get my renewal, go through it to ensure there aren't major changes, the price is reasonable based on the previous premium and then renew.

Sounds familiar? You get your mortgage renewal, too busy with kids, work and life, numbers look ok and you renew? I wasn't happy with the increase in premium and decided to look around.

I tried a price comparison site which provided a low price but after connecting with the insurance company it turned out the information transferred to them from the rate site was inaccurate and the quoted price was invalid; it was higher.

Sounds familiar? You check out a mortgage rate site to find out the rates being quoted are for 30 day closings, have restrictive conditions, not valid for rental properties, you can't refinance the mortgage in the future.....and the list goes on.

By investing some time I saved 25% off what was offered by the existing insurance company.

Don't sign the renewal letter sent by your incumbent lender

Rate sites provide a number but don't tell the full story

Take the time to consult with a professional, it could save you thousands of dollars

In my business, new and repeat clients are provided with superior service and their business is never taken for granted. I don't understand why some businesses take their existing clients for granted.

If your mortgage is up for renewal, you don't want to be taken for granted and looking for professional unbiased advice, please contact me.

There have been many changes with respect to mortgage qualifications in Canada. Above and beyond the 4 major changes announced by the Minister of Finance over 4 years, there have been changes on the backend on how lenders qualify applicants. The most recent one is mind boggling!

For an applicant reporting a surplus on their T1 general (line 126), the surplus (line 126) is added to their income.

Example: Applicant's income is $100,000 and line 126 is showing $5,000, total applicant's income is $105,000. If the applicant owns other investment properties, here is the part that makes no sense: The principal portion off the annual mortgage statement is deducted from applicant's income!

Example: Applicant has paid down $10,000 of mortgage principal in the previous year, total income: $100,000 plus $5,000 less $10,000 = $95,000. This rule effectively penalizes real estate investors who build equity in their investment properties. Last time I checked statements made by Minister of Finance, Bank of Canada, Bankers..... they all advocate paying down debt and building equity now while interest rates are low (Canadians are at record high debt to income ratio).

This rule effectively encourages not paying down mortgage principal. Had the applicant paid more interest than principal in the previous year, the mortgage principal deduction would have been less and therefore their net income higher!

If you are thinking of showing a loss on line 126, it's even worse: Income less loss on line 126 less mortgage principal.

Are you confused and frustrated with all these guidelines? Rest assured this is what I do on a daily basis and I am here to help you navigate through the mortgage qualification land mines to build your real estate investment portfolio. It's all in the setup.....Happy Investing!

Want to Invest In Real Estate But Not Sure Where To Start? - Nawar Naji Toronto Mortgage Broker