I know, this is against what I stand for: achieving mortgage freedom and building long term wealth, but let me explain why 30 year amortization mortgages are good. The exception is for home buyers putting less than 20% downpayment, the maximum allowed amortization is 25 years per government requirements.

Why 30 Year Amortization Mortgages?

Lately, I have been coming across clients where certain events have dictated changes in their housing situation:

- A couple where one spouse has gone back to school to upgrade their skills. The are down to one income for a few years. Having 30 year amortization mortgage instead of 25 year amortization mortgage makes a difference in their cash flow requirements.

- A first time home buyer who wants to move up the home ownership ladder by renting their existing home instead of selling. Having a 30 year amortization mortgage would improve the cash flow on the income property (current home) which helps in qualifying for the next home.

- A couple where one spouse has lost their job and have young children. This is another case of a 30 year amortization mortgage would make a big difference for cash flow purposes.

- A homeowner who bought a home with 25 year amortization mortgage is looking to move prior to mortgage maturity. To save client penalty money, my recommendation was to port mortgage and increase mortgage amount. However since original mortgage is amortized over 25 years, they qualify for a lower amount than they desire.

- Real estate investors who got financing through institutions that required investment properties to be amortized over 25 years are having issues acquiring further properties since 25 year amortization mortgages result in lower net cash flow.

With today's low interest rates, porting a mortgage and doing and increase & blend will be more popular in the future. It doesn't make sense to break a mortgage at 2.99% in 3 years from now. Having a 30 year amortization mortgage provides the qualification flexibility for future moves.

Mortgage Freedom

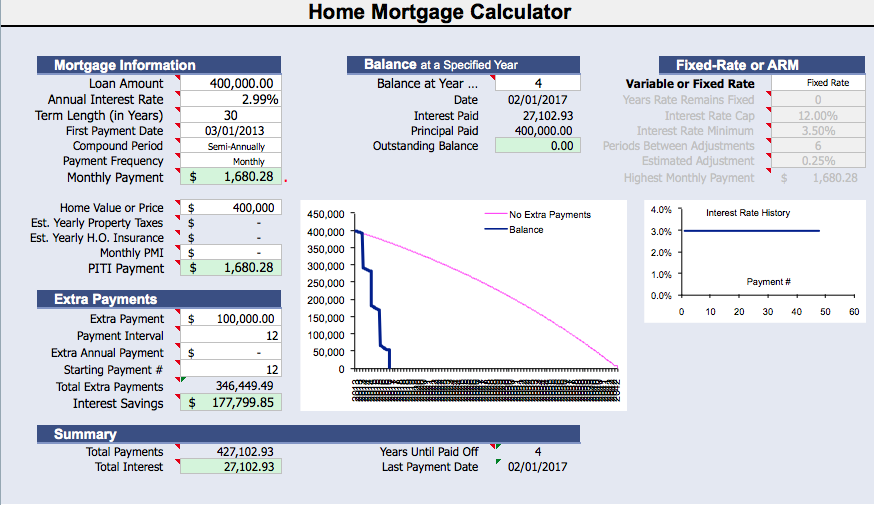

I have arranged mortgages for clients who wanted to amortize their mortgage over 10 years. So how can a 30 year mortgage be paid off in less than 10 years? Mortgages, typically, come with 20% pre-payment privileges. If the homeowners utilize this privilege they can be mortgage free in less than 5 years by applying the 20% pre-payment privilege every year. Here is an example:

{kind=link}

Mortgage Amount: $400,000 Mortgage Interest Rate: 2.99% Annual Pre-Payment: $100,000 Mortgage paid off in 4 years

I realize the above example is extreme, where very few homeowners can pre-pay $100,000 annually of after tax dollars. This example illustrates homeowners shouldn't focus on shorter amortization mortgages since the pre-payment feature is a more powerful tool.

Oh and you can still get a 35 year amortization mortgage in Canada today!

To discuss your mortgage financing needs whether you are buying a home, an investment property or renewing your mortgage, please contact Nawar.